Dentium 2025 Q4: Net Profit Turns to Loss, China Region Revenue Drops 25%

|

| Image Source: Dentium 2025 Q4 Business Performance Report |

Q4 Revenue 109.1 Billion KRW / China Market Revenue Down 25% / Vietnam, India & Other Asian Markets Revenue Up 87%

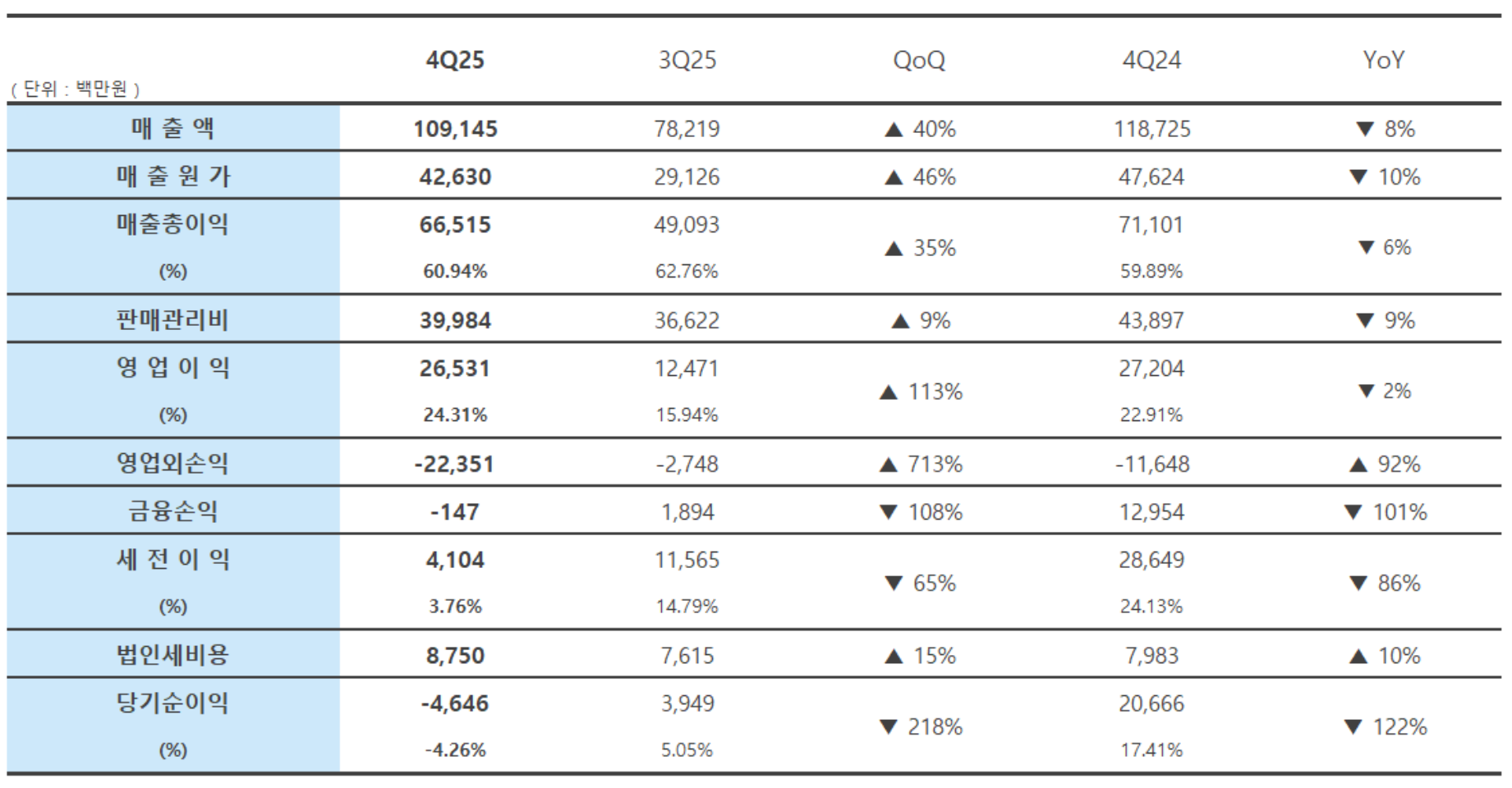

DentalGoodNews|South Korean dental implant company Dentium has released its financial report for the fourth quarter of 2025. The report shows that the company achieved revenue of 109.1 billion KRW (approximately 510 million RMB) in Q4, a year-on-year decrease of 8% and a quarter-on-quarter increase of 40%. Operating Profit was 26.5 billion KRW (approximately 124 million RMB), a year-on-year decrease of about 2% and a quarter-on-quarter increase of 113%. Affected by one-time factors such as asset impairment of overseas subsidiaries, the company's net profit for the quarter was -4.6 billion KRW (approximately -22 million RMB), a 122% decrease compared to 20.6 billion KRW (approximately 96 million RMB) in the same period last year, and a 218% decrease quarter-on-quarter.

The company stated that the Q4 revenue decline is mainly related to weak demand in the Chinese and domestic South Korean markets. While market competition intensified, the weakening macroeconomic environment led to a phased contraction in dental implant demand. However, the Chinese market is expected to gradually recover as the Volume-Based Procurement (VBP) 2.0 policy is gradually implemented.

|

| Image Source: Dentium 2025 Q4 Business Performance Report |

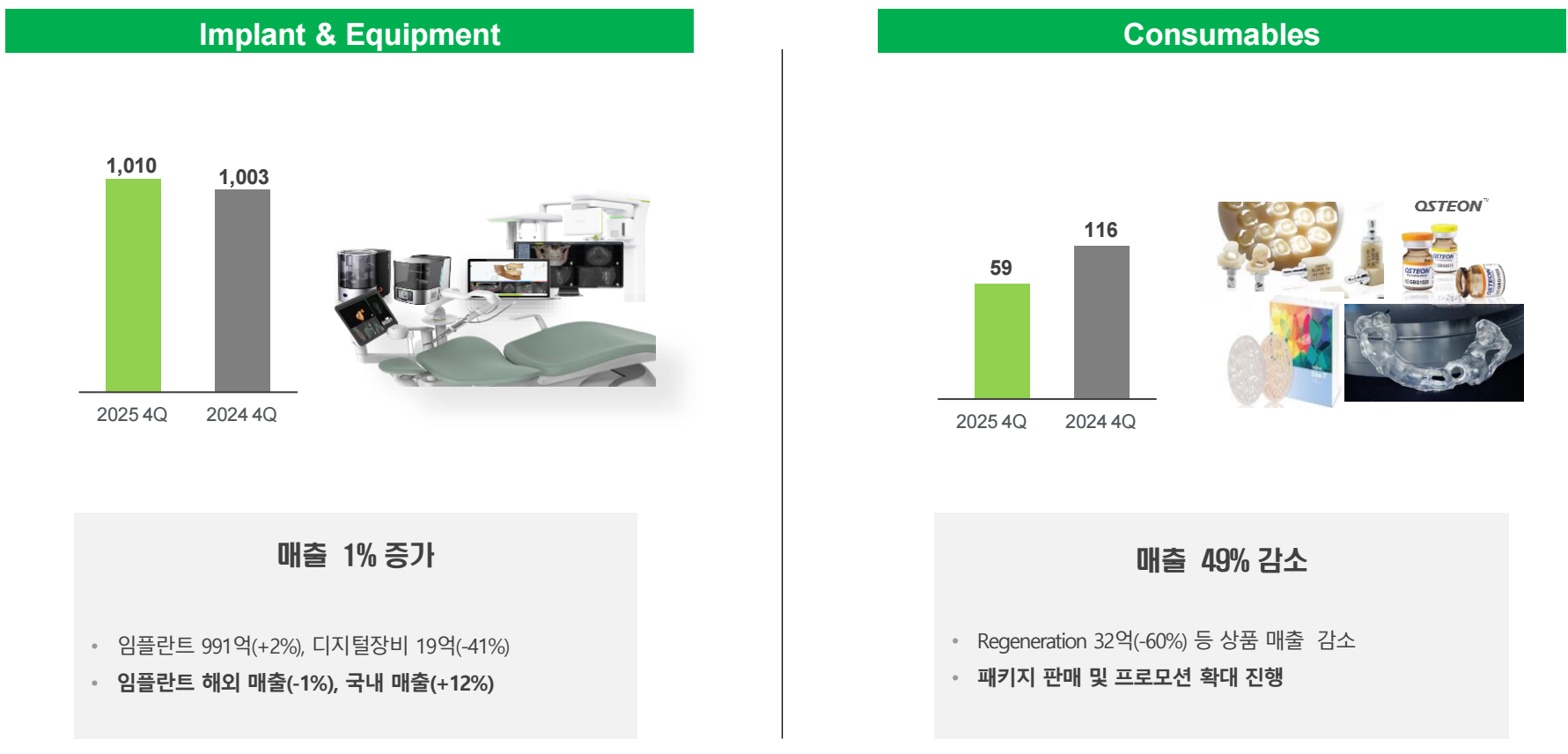

From a business structure perspective, revenue from the Dental Implant and equipment business in Q4 was 101.0 billion KRW (approximately 473 million RMB), a year-on-year increase of 1%. Revenue from the Consumables and Regenerative Materials business was 5.9 billion KRW (approximately 28 million RMB), a year-on-year decrease of 49%, mainly due to reduced sales of Regenerative Materials and changes in the product mix. Specifically, Dental Implant business revenue was 99.1 billion KRW (approximately 464 million RMB), a year-on-year increase of 2%; Digital Equipment revenue was 1.9 billion KRW (approximately 8.9 million RMB), a year-on-year decrease of 41%. The company noted that overseas sales of implants saw a slight year-on-year decline, but domestic sales in South Korea achieved 12% growth.

|

| Image Source: Dentium 2025 Q4 Business Performance Report |

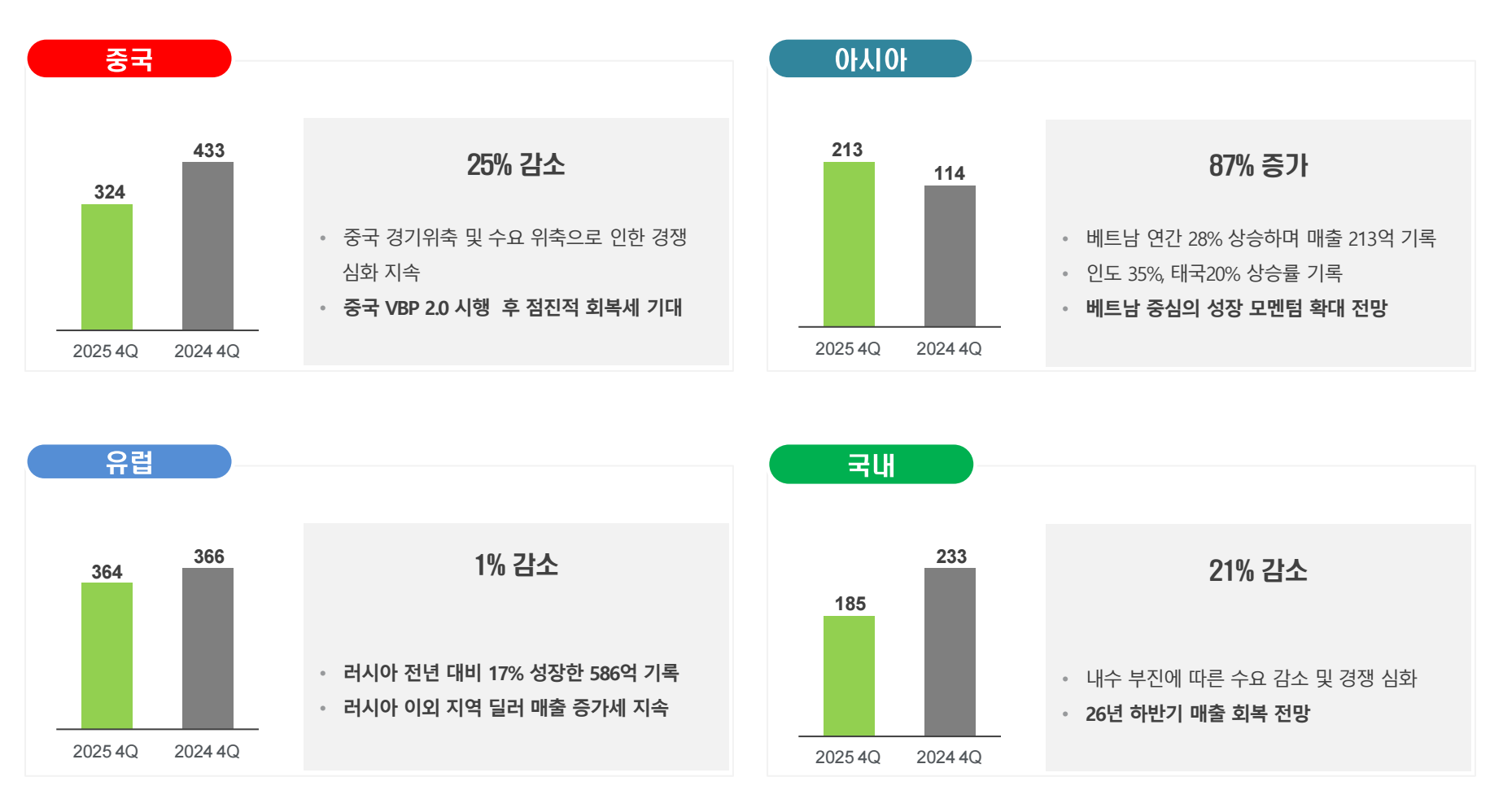

From a regional structure perspective, Q4 revenue from the Chinese market was 32.4 billion KRW (approximately 152 million RMB), a year-on-year decrease of 25%, primarily affected by economic slowdown and weak demand. Revenue from other Asian markets was 21.3 billion KRW (approximately 100 million RMB), a year-on-year increase of 87%, with significant growth in Vietnam, India, and Thailand. Vietnam's full-year revenue increased by approximately 28% year-on-year, becoming a key driver of regional growth. The Indian and Thai markets achieved growth of about 35% and 20% respectively. The company expects the Southeast Asian market, with Vietnam at its core, to continue to be a significant driver of future growth.

The European market remained generally stable. Q4 revenue was 36.4 billion KRW (approximately 170 million RMB), essentially flat year-on-year (-1%). Within this, the Russian market grew by about 17% year-on-year, helping to maintain steady regional performance. The domestic South Korean market saw a decline, with Q4 revenue of 18.5 billion KRW (approximately 87 million RMB), a year-on-year decrease of 21%, mainly due to weak domestic demand and intensified market competition. The company expects a gradual recovery in growth in the second half of 2026.

|

| Image Source: Dentium 2025 Q4 Business Performance Report |

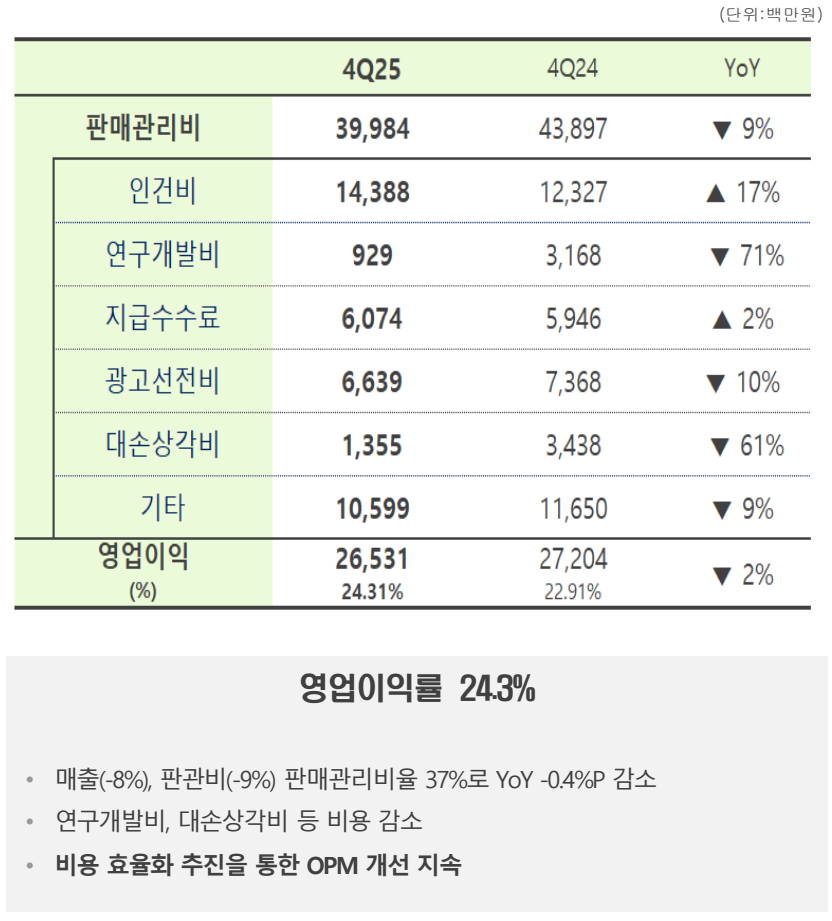

From an expense structure perspective, the company's Q4 selling and administrative expenses were 39.984 billion KRW (approximately 187 million RMB), a year-on-year decrease of 9%. The selling and administrative expense ratio for the reporting period was approximately 37%, down 0.4 percentage points from the same period last year. Specifically, labor costs were 14.388 billion KRW (approximately 67 million RMB), a year-on-year increase of 17%; R&D expenses were 929 million KRW (approximately 4.3 million RMB), a year-on-year decrease of 71%; payment processing fees were 6.074 billion KRW (approximately 28 million RMB), a year-on-year increase of 2%; advertising and promotion expenses were 6.639 billion KRW (approximately 31 million RMB), a year-on-year decrease of 10%; and bad debt provisions were 1.355 billion KRW (approximately 6.3 million RMB), a year-on-year decrease of 61%.

Against the backdrop of year-on-year revenue decline, the company drove down expenses by compressing R&D expenses, advertising expenses, and bad debt provisions, while continuing to advance cost efficiency optimization. This led to an improvement in the Operating Margin to 24.3%, up from 22.9% in the same period last year.

|

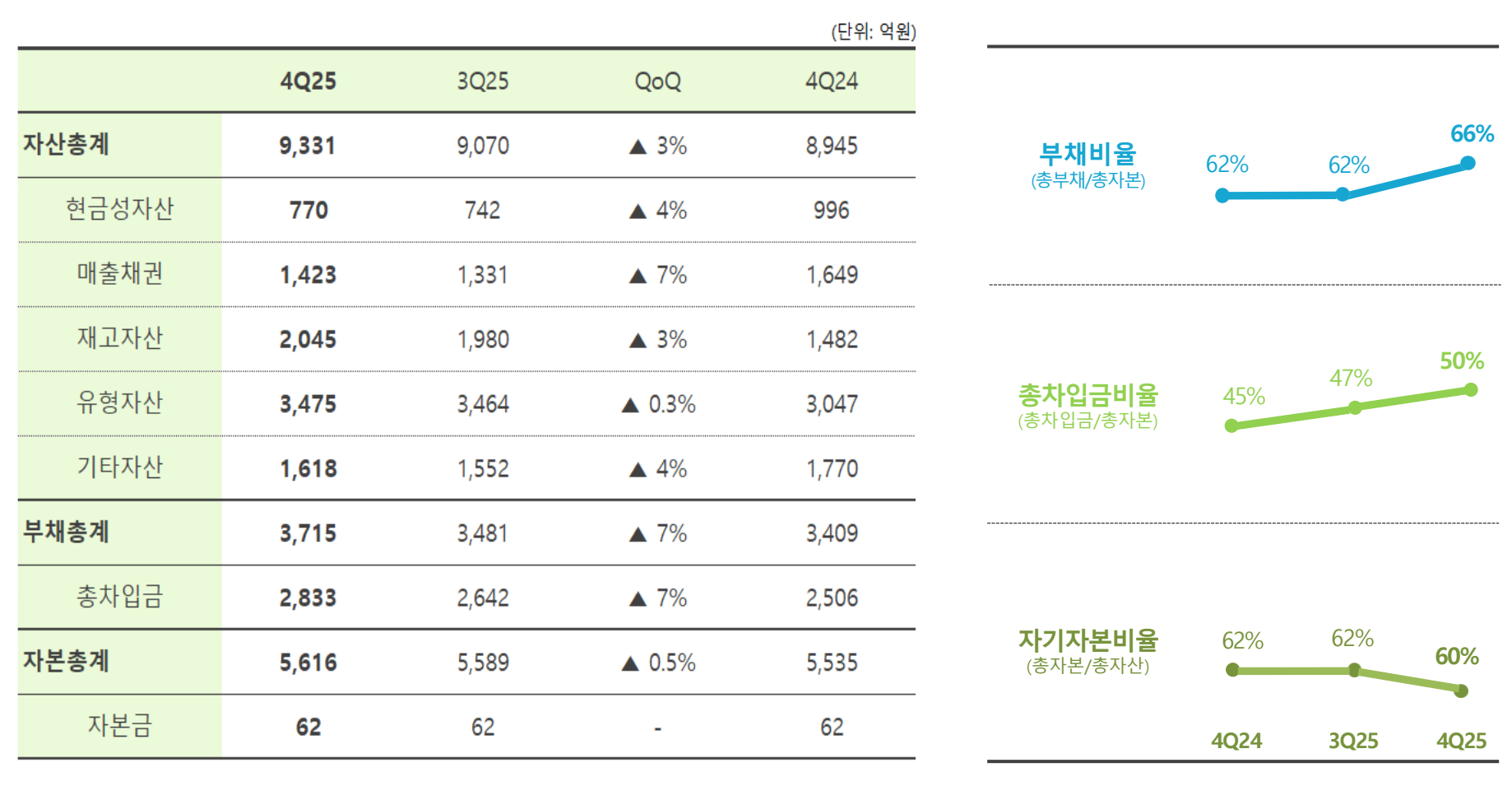

| Image Source: Dentium 2025 Q4 Business Performance Report |

Regarding assets and liabilities, as of the end of Q4 2025, the company's total assets were 933.1 billion KRW (approximately 4.366 billion RMB), an increase of about 4% compared to 894.5 billion KRW (approximately 4.186 billion RMB) in Q4 2024, and a 3% increase quarter-on-quarter compared to Q3 2025. Among these, cash and cash equivalents were 77.0 billion KRW (approximately 360 million RMB), a quarter-on-quarter increase of 4%; Accounts Receivable were 142.3 billion KRW (approximately 666 million RMB), a quarter-on-quarter increase of 7%; and inventory was 204.5 billion KRW (approximately 957 million RMB), an increase of about 3% from the previous quarter.

On the liability side, the company's total liabilities at the end of Q4 were 371.5 billion KRW (approximately 1.738 billion RMB), a year-on-year increase of about 9% and a quarter-on-quarter increase of 7%. Among these, total borrowings were 283.3 billion KRW (approximately 1.326 billion RMB), a year-on-year increase of about 13%. Total Shareholders' Equity was 561.6 billion KRW (approximately 2.628 billion RMB), a slight increase from 553.5 billion KRW (approximately 2.590 billion RMB) in the same period last year.

From a financial structure perspective, the company's asset-liability ratio at the end of Q4 was 66%, up from 62% in Q4 2024; the Total Borrowing Ratio was 50%, up from 45% in the same period last year; and the Equity Ratio was 60%, slightly down from 62% in the same period last year. The overall capital structure remains relatively stable.

| About DGN:DentalGoodNews (DGN) is a trusted professional media platform dedicated to the global dental industry. We deliver in-depth coverage of corporate news, policy & regulation, investment & funding, and clinical frontiers — serving dental institutions, device manufacturers, investors, and industry researchers worldwide. Contact us: haodeya@dongxizixun.com |

;){kind=link}